According to Fundera 20% of small businesses fail in their 1st year, 30% in their 2nd, 50% in the 1st 5 years and 70% in the first 10. Those failure rates are probably higher for those trying to build a brand, as ‘small businesses’ often include one-man-bands, consultants etc.

There are hundreds of reasons why business fail; competition, pricing, team, capital etc.

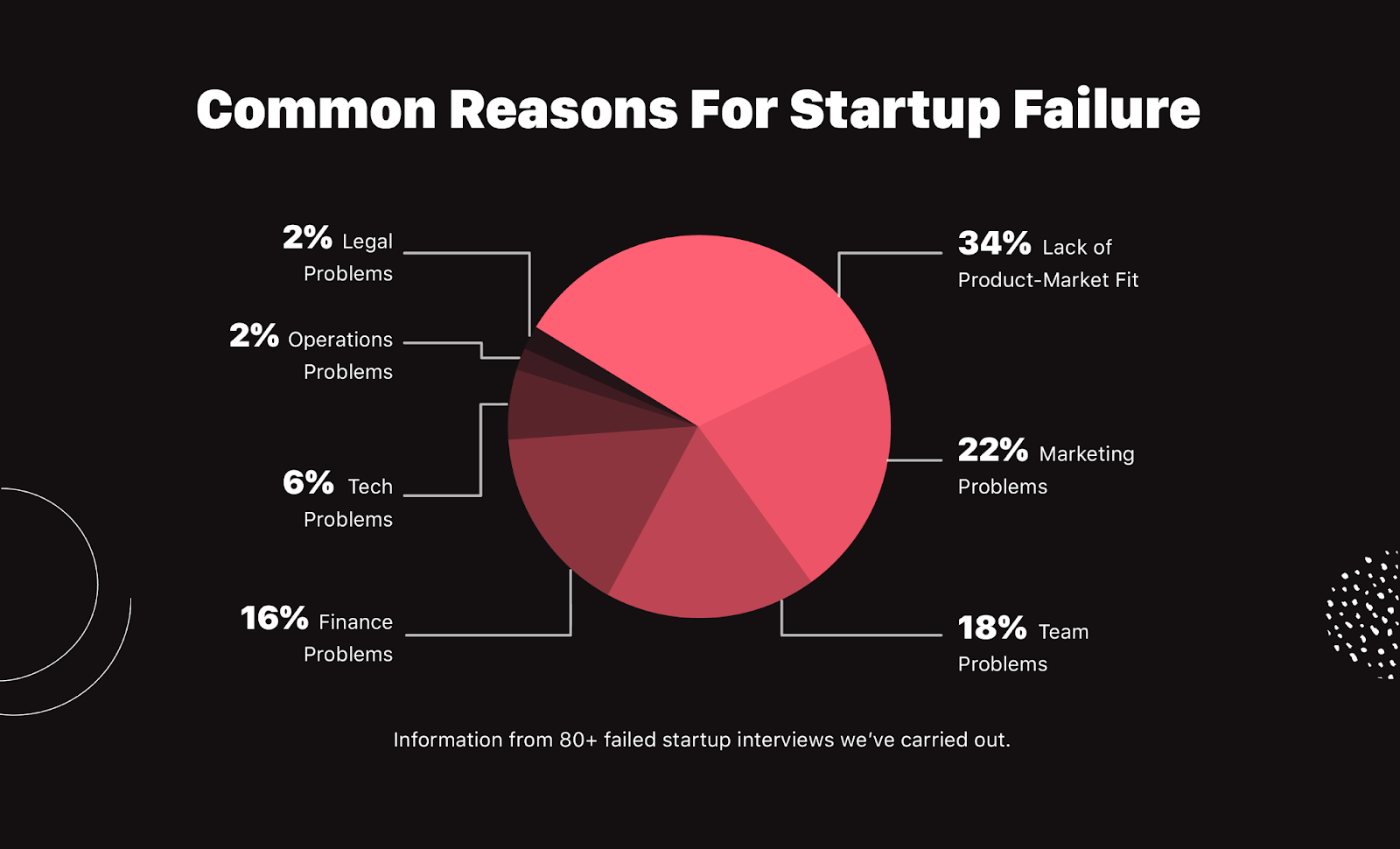

(Graphic above from https://www.failory.com/blog/startup-failure-rate)

There are plenty of articles about this, but what I haven’t seen anything written about is “knowing the rules of the game”. When you don’t know the rules of a game it’s easy to lose and impossible to win.

If you watch Dragon’s Den (which is becoming further and further away from the real-life way of doing business… but that’s a separate post) you would think start-ups should be fast-growing and profitable, and that seems pretty logical. Then if you look at some of the biggest, most famous companies in the world (Amazon, Tesla, Uber, Airbnb etc) they were all loss-making for a long period of time and many still are. So what is going on? Are the all-knowing Dragons wrong?

Looking at a sector that I know well, pet food, in 2017 tails.com had a turnover of £13.4m with losses of £2.8m (figures from Companies House). You would think that those losses would inspire a very quick “I’m out” from the Dragons, but what actually happened was that Nestle bought the company for reportedly over £110m. That’s right, a valuation of nearly 10x turnover for a company with nearly £3m losses… a great payday for investors like JamJar and Octopus Ventures who backed them, but why was Nestle ‘in’? Tails went on to make a £7.2m loss on £23.6m sales in the 14 months to Dec 2018 and an £11.5m loss on £32m of sales in 2019, so Nestle obviously like the strategy.

Another pet food company, Butternut Box (Dogmates ltd on companies house) shows losses of £5.5m on £3.6m sales in 2018 and £7.9m losses on £10.9m sales in 2019. Another “I’m out”? No, based on these figures they raised a reported £15m investment from L Catterton in 2020, bringing total investment to a reported £41m.

So what is going on? To anyone brought up on a diet of Dragon’s Den and Monopoly, none of this makes any sense.

The answer is that the people behind these companies know the real game and how to play it. One co-founder at tails.com came from Lovefilm, which sold to Amazon for £200m, another came from Innocent, which sold to Coca-cola for a reported £320m. Both co-founders at Butternut Box came from Goldman Sachs. They know how the system works; which type of companies invest, at what levels, what they are looking for, what their exit plans should look like, how investors make their money and much more.

The trend holds true with bigger companies. Jeff Bezos worked at investment firm DE Shaw before starting Amazon. Elon Musk sold Zip2 (no I hadn’t heard of it either) to Compaq for $307m before founding x.com, which merged with PayPal and then gave him the knowledge to build Space X and Tesla (loss-making for 15+ years).

They all know the rules of the game and how to play it.

So, what are the rules?

To be honest, I am not on “the list” and have never taken any money from an institutional investor (although I have discussed the opportunity with many). We have received outside funding, but that was from a trade deal, not an institutional investor and that’s not the same game, and not the same rules. However, from what I have learned over the years this is what I think the rules might be:

1) Understand who wants what and why

Investors want to make money, that’s pretty simple. However, EIS/SEIS investors might want you to do crazy growth or die trying – those investors can be financially better off if you go bust, rather than have steady growth if no one wants to buy their shares. Most institutional investors have a timeline for their funds, this needs to fit your timeline for your business. Most funds have a clear mandate and you need to make sure your investment opportunity matches their mandate. In this game you need a model that matches what the people who hold they keys to the treasure chest want.

2) Know how your destination

Investors only make money when people buy their equity. An EIS investor may be bought out by a PE, a PE may be bought out by another PE, they may be bought out by a bigger trade player, or they may exit in an IPO. You need to know how other deals in your sector have played out, what multiples/valuations companies got and therefore what your potential future will be. Referencing the examples above; tails.com could be confident that a big player like Nestle would buy them if they got big enough and were disruptive enough in a category that Nestle already operated in and they knew Nestle would look at topline sales and growth over profitability, so that’s what they based their model on. Butternut Box are following the same path. If you’re in a sector that doesn’t have a big player likely to buy you and your investor out, how would your investor get a return? You need to know.

3) Understand the different types of investor

JamJar have a great page on this (http://www.jamjarinvestments.com/tips) and there is no point in me repeating, but suffice to say not all investors are the same. A VC is likely to want very high growth and will look at burn rate and growth rate, possibly not much else, very likely not bottom-line profit. Some PE’s on the other hand won’t even look at you if you don’t show profit. You need to pick the right funding for your business model. As a VC said to me recently, “you need to pick what temple you want to worship at, and we worship at the temple of growth”.

4) Scale: It’s all down to basic maths

Most of the companies that get sky-high valuations on loss-making businesses do so because they have proven that they can scale. They tend to offer relatively simple products and the goal is to sell more of those products, usually online. This tends to come down to some pretty simple maths. Let’s say at early stage you can show that your product costs £10 per month and the average retention of a customer is 1 year, so your LTV (lifetime value) is £120 (12 months x £10). Your gross profit on the £120 is 50%, so £60. Your CPA (cost per acquisition) is £20. Effectively this means your business is an engine to turn £20 into £60. That means if an investor gives you £200,000 you should be able to turn it into £600,000. Once you’ve proved that another investor will give you £2,000,000 and you should be able to turn it into £6,000,000. Once you’ve proved that another investor will give you £20,000,000 and you should be able to turn it into £60,000,000. And so on. Obviously, this is a massive oversimplification (you need to account for people, premises, stock, cashflow etc), but you get the point, and if you can prove the maths you’ll get the investment.

Those may (or may not) be the rules, but there is also the reality:

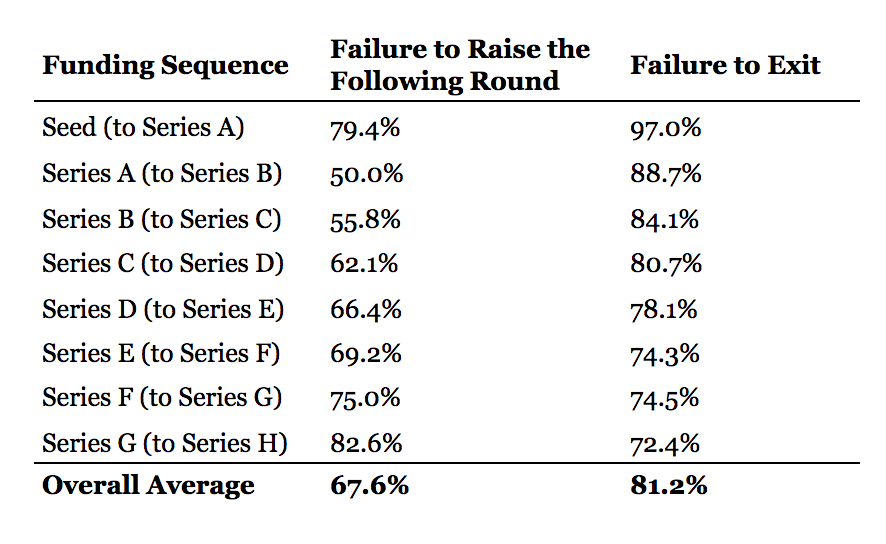

1) According to these stats VC-backed start-ups have a lower chance of success.

(Table above from https://medium.com/journal-of-empirical-entrepreneurship/dissecting-startup-failure-by-stage-34bb70354a36 )

2) “lifechanging” deals may not be lifechanging

Even if the company that you found gets backing and is “successful” that doesn’t necessarily benefit a founder. You could successfully raise a fundraising round that values your stake in the company at £millions, but try using that valuation to get a mortgage to buy a house (good luck!) and your likely to take a lower salary than you could expect to be paid working for someone else because your investors most likely want the money to go into the company, not your pocket, and you accept this because of the potential future value of your equity (which according to the point above has an 80% chance of never materialising).

3) You only hear the hype

Generally, the stories that you hear about sky-high valuations are the exceptions rather than the rule. Most companies will never achieve them and if they do there’s always the small print of the deal that you don’t get to read.

You hear a lot less about the companies that grow nicely, doing a very good job, and who are likely to be around for a lot longer, or about the companies that change hands for £1 and that is considered a good deal. Those happen far more than the sky-high deals, but they aren’t very newsworthy and the companies involved don’t have the PR budgets of the ones who just raised a fortune.

4) A small percentage of something bigger isn’t always better

One of the things the institutional investors and the Dragons would agree on is, “you’re better to have a 10% share of a £50m company than a 100% share of a £5m company”, but are you? For some people yes, but with a 10% share of a £50m company you are responsible to your investors and effectively working for someone else. With a 100% share of a £5m company you are truly in charge, you can do what you want and don’t have the stress of dealing with investors. Neither is right or wrong 100% of the time and there is a lot of grey area in the middle, it depends on the individual.

People who have ‘cut their teeth’ at investment banks and big brands tend to play to the rules a lot better than many of the entrepreneurs who have built their businesses through passion, wit, guile and very little formal training. These entrepreneurs in the words of Cranfield Business School are often “The Unemployables”, or as my wife says, “don’t play well with others”.

Then there is the biggest rule of all… there are no rules really. You don’t have to follow anyone else’s path. As Fleetwood Mac say, “You can go your own way”.